The Gaps and Traps of Overnight Trading

Swing trading looks controlled during market hours. A position is entered with a thesis, a chart, a stop, and a target. Risk appears measurable because the trader can still react. The order ticket is open, the tape is visible, and the market can be watched in real time. Once the closing bell rings, that control changes. The trade does not stop, but the trader’s ability to manage it does. That is the swing trader’s dilemma. During the trading day, the position is under active management. Overnight, it becomes passive exposure. Capital remains fully at risk, yet the trader is no longer operating in a live decision loop. News can break, counterparties can reprice risk, overseas markets can move, and the next print in the stock may be nowhere near the last price seen at the close. At the same time, swing trading does not have a sufficiently long time-horizon for the trader to confidently ignore movements that a position trader or investor would label noise or insignificant short-term trends.

This is where the idea of continuity matters. Markets are often spoken about as if they are always functioning, especially now that headlines move across screens every minute. But listed equities are not truly continuous markets. News is continuous. Pricing is not. There are openings and closings, stretches of thin extended trading, and large gaps where information accumulates faster than it can be traded. That mismatch is the source of much of overnight risk. For swing traders, the problem is not just finding a clean setup. Plenty of people can find a breakout, a pullback, or a trend continuation. The harder part is surviving the hours when nothing can be adjusted with normal precision. A trade can be right on structure and still turn ugly by the next open. In practice, swing trading success depends as much on surviving off screen risk as it does on timing an entry.

Overnight trading risk is not a side issue in swing trading; it is part of the job. The trader who wants to profit from multi-day trends has to accept periods when positions are exposed but not actively managed. That is the bargain. The reward is regular access to larger moves than a typical intraday strategy will capture.

The mistake is not taking overnight risk. The mistake is pretending it can be managed the same way as normal intraday volatility. It cannot. You need to take serious slippage and liquidity drops into account, and understand how macro news can hit every correlated name at once. None of this is rare enough to ignore, and good swing traders respect that reality. They size positions so one bad open does not wreck the month. They treat earnings and scheduled catalysts with caution. They use options when defined risk is worth the cost. They build portfolios that can survive being wrong overnight. That is what separates a solid swing process from an expensive hobby. Entries matter, no question. But staying solvent and composed between one close and the next matters more than most traders like to admit. Trade the plan and respect the gap.

The Core Risk: Price Gapping

What a gap actually is

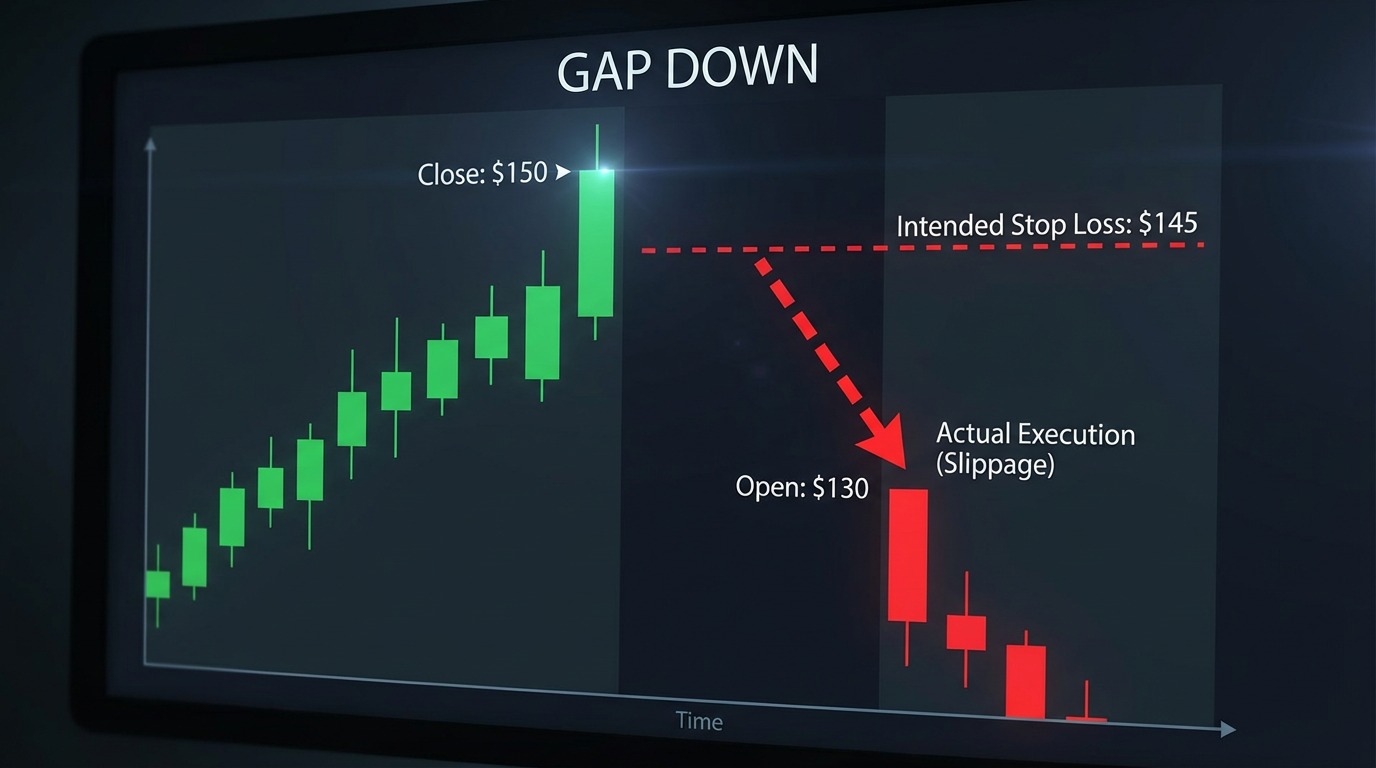

A gap occurs when a stock opens at a price materially different from its previous closing price. The dangerous cases are the large ones, where new information forces a sudden repricing. A stock that closed at $150 may open at $144, $135, or even lower if the overnight news is bad enough. The chart shows empty space because no regular session trading happened in between.

Gaps matter because they break the normal rhythm of trade management. Intraday volatility is often noisy but tradable. A stock drops, support is tested, bids appear, and an exit can be taken with some degree of discretion. Overnight repricing skips that process. There is no slow slide through each price level. One moment the position is marked at the close, the next it is being valued at the open, often after a flood of new information has already reset expectations.

Slippage and the stop-loss illusion

Many new swing traders misunderstand stop-losses and this misunderstanding ends up being expensive for them. A stop-loss order is not a price guarantee. It is an instruction to place a sell order (if you are long) once the market trades at or through a trigger point. If a stock closes at $152 and trader has placed a stop at $150 for a long position, that sounds neat on paper. The assumption is that the worst possible outcome is a sale at $150 or just slightly below. That assumption fails the moment the stock opens at $135.

In that case, the stop is activated into a market that no longer exists at the planned level. The order will execute at the next available price, which may be far below the stop-loss point. This difference between the intended exit and the actual execution price is called slippage. During fast overnight repricing, slippage can be severe. The trader did manage risk, but in theory only.

That is why stop-loss orders alone is not a complete overnight risk plan. Stops still matter, but they are no the only tool in the toolbox. They are useful for containing ordinary session losses, and much less reliable against discontinuous moves caused by major news.

Why the move can be so violent

The events that create these gaps are often binary. An earnings report can reset forward revenue assumptions, margins, guidance, and valuation multiples in one go. The market is not adjusting by a few cents. It is rebuilding the price around a new view of the business. The same applies to regulatory shocks. A disappointing FDA decision can seriously damage the value of a biotech name in a single morning if the company’s future cash flow was tied to one product approval. At the larger macro end, geopolitical shocks, sanctions, military escalation, or a sudden policy surprise, can trigger risk off behavior across sectors before the trading session even starts.

These are classic traps of overnight trading. The trader goes to bed after setting a stop-loss, and then wakes up to a very different number. The market repriced faster than the strategy could respond. That is normal in overnight trading, which is exactly why it has to be treated with more respect than many simple chart based strategies suggest.

How can stock prices move when the market is closed?

How can a stock traded at the New York Stock Exchange (NYSE) close at $85 and open at $80 the next day?

The opening price for the regular session is derived from matching orders that accumulated overnight. Example: The regular session closes at $85. Overnight, bearish news comes out. Lots of sell orders pile up. At the next open, the exchange matches orders at the best price where supply meets demand. This happens before the regular session opens. In this case, it resulted in an open price of $80 for the stock. That is known as a gap down. If the price had gone from $85 to $90 between close and open, it would have been a gap up.

Other exchanges have similar routines, although the exact rules can vary. Below, we will take a more detailed look at how the opening price is determined at NYSE.

How opening stock price is determined at NYSE

- At NYSE, the pre-open period (aka pre-market auction or opening auction) usually starts a few minutes before 9:30 am ET (exact timing varies). During this time, orders accumulate, including both market orders (buy/sell at any price) and limit orders (only buy/sell at a specific price). No trades are executed yet, but the system is collecting and analyzing supply and demand.

- The next strep is price discovery. The exchange calculates the single price that maximizes matched orders. This is the official opening price, sometimes called the “auction price”.

- Once the opening price has been determined, the exchange executes all matched orders at that price simultaneously.

- Then the regular session begins at 9:30 AM ET.

As you can see, the actual price matching happens before the market opens, not during the first active trades. The first trade of the session is technically the result of the pre-market opening auction, so any “gap up” or “gap down” is already reflected at 9:30 am.

If there’s very low liquidity overnight or unusual order imbalance, NYSE can delay the opening slightly to find a fair price, but the price is still set before continuous trading begins.

Understanding the role of pre-market and after-hours trading (extended-hours trading)

Pre-market and after-hours trading are also concepts that a swing trader should know about and take into account. Many exchanges have an after-hours session right after close and a pre-market session right before open. These sessions typically have fewer participants, lower liquidity, and wider spreads. Because of that, even small trades can move prices significantly.

Access to pre-market and after-hours trading (often called extended-hours trading) is broader than most people think, but not everyone participates in the same way. The main players are the institutional investors, such as investment banks, hedge funds, mutual funds. They have vast amounts of money to move, and they dominate the extended-hours trading and react very quickly to news. Their resources, including advanced trading software and liquidity access, are supreme. When a significant gap happens, it is because these players have changed their sentiment.

Retail traders can also access extended-hours trading, especially in the United States where many retail online brokers offers extended-hours trading even to small-scale hobby traders. Examples of such brokers are Robinhood, Interactive Brokers, TD Ameritrade, and E*TRADE. For retail traders, brokers will typically only allow limit orders (only buy/sell at a specific price), and the list of stocks can also be reduced compared to main session trading. Only allowing limit orders is a way to protect retail traders, because during extended-hours trading, market orders can execute at absolutely horrible prices. This is a consequence of the reduced liquidity and lower number of participants.

Extended-hours trading is very common in the United States, where it is also widely accessible through brokers. In the rest of the world, it is less common and less standardized. Where it exists, it is often more limited than in the United States, and can be more difficult for retail traders to access.

In the United States, the typical pre-market session is 4:00 am to 9:30 am (ET), and the typical after-hours session is 4:00 pm to 8:00 pm (ET). Examples of exchanges that stick to this schedule are NYSE, Nasdaq, Cboe BZX Exchange, and IEX.

What a retail trader gets access to will also depend on the broker, as some brokers limit retail access to extended-hours trading based on a combination of liquidity and infrastructure constraints.

Should a retail swing trader participate in extended-hours trading?

Even when extended-hours trading is available, many traders opt out because of the low liquidity (more difficult to predict where you can enter and exit), the wide spreads (which means higher costs for the trader), and the higher volatility (expect sharp and unpredictable moves). Institutional traders and other professional traders are more likely to seek out extended-hours trading, even though retail traders also have access.

Extended-hours trading can still have its place in a retail swing trading strategy, but only when used very selectively. For most successful retail swing traders, extended-hours trading is a tool for special situations, not a default habit. It can help in specific situations (especially around news), but it also introduces its own risks and issues. And the mere fact that it is not a part of your habitual trading will also increase risk, since you will not be used to the different dynamic and psychological challenges of extended-hours trading.

Getting involved in extended-hours trading will give you the opportunity to react quicker to news. Many companies report outside the main trading sessions, and swing traders who don´t participate in extended-hours trading have to wait by the sidelines. There are also other types of news that impact stock prices, and these news can of course happen at any time of day or night.

The lower liquidity and higher volatility changes the dynamic significantly, and you should prepare yourself for displeasing fills on your limit orders. You may for instance get partially filled, or get filled just before a reversal. The situation tend to be even worse for stocks that are not large-cap.

Using extended-hours specifically to react quickly to news instead of letting a pre-decided strategy play out during regular sessions increases the risk of emotional trading, e.g. panic selling, chasing losses, and just general overtrading.

Extended-hours trading can be used as one of several tools to manage overnight gap risk, but will not eliminate it. You can for instance (usually) exit or trim positions after bad earnings news, but you might not get the price you hoped for, since institutional traders will react faster and slippage can be brutal. You might still take a big loss, just earlier than if you had waited for the regular session. Sometimes you’ll actually get a worse price, because markets sometimes correct themselves before or shortly after opening. Also factor in the wider spreads.

Extended-hours trading can give the impression that the market remains open enough for risk to be managed. Sometimes it does, but often it does not. As discussed above, after-hours and pre-market sessions are much thinner than the regular session. Fewer participants are active, spreads are wider, and price discovery is less stable. This means smaller orders can move price more than traders expect and it also amplifies reactions to news. A disappointing report released after the close can send a stock sharply lower not only because the news is bad, but because there are fewer bids available nearby. The print seen at 5:15 p.m. may not reflect where a deep regular session market would have priced the stock. It reflects where a thin extended market found enough liquidity to transact.

For traders, including swing traders, that creates two major problems. First, the mark to market swing can look extreme and still be real enough to shape sentiment by morning. Second, attempting to exit in thin conditions can itself produce a poor fill. A trader trying to reduce overnight damage may be forced to hit wide spreads in a market with limited depth. That is often better than freezing, but it is not the same as having full session liquidity.

Understanding the Catalysts of Overnight Volatility

Corporate earnings and company specific news

For individual stocks, earnings are the clearest and most consistent source of overnight volatility. They are scheduled, widely watched, and often capable of producing double digit percentage moves in a single session transition. Even when a company beats estimates, the stock may still sell off if guidance disappoints or management signals weaker demand. The reverse also happens. A mediocre quarter can be forgiven if forward commentary improves.

Earnings are dangerous for swing traders. The event is known in advance, but the market reaction is not. Price action into the report may look strong, weak, or neutral, but once the numbers hit, the old chart can become almost irrelevant. Traders often talk about “playing the setup” into earnings, but in reality the position becomes a short term bet on how expectations compare with reported data and management guidance. That is not the same thing as a normal swing trade.

Even when extended-hours trading is available, the depth is often poor relative to regular session volume. A stock may swing sharply in response to the release, then move again during the conference call, then gap a second time at the open once institutional positioning kicks in. Traders sometimes think they will react after the headline, but the headline is only the opening act. The real repricing may continue for hours.

Economic data and macro releases

Not all overnight risk is company specific and a stock does not need bad company news to gap lower.

Economic releases can move entire sectors or the full market before the opening bell. Inflation data, payroll numbers, central bank decisions, GDP prints, and purchasing manager surveys can all alter interest rate expectations, recession odds, and risk appetite. When that happens, a swing trader holding an otherwise sound position can still get hit because the whole market regime shifts before the session begins. A stronger than expected inflation print can raise bond yields, compress valuation multiples, and pressure growth stocks in one go. A weak payroll release can trigger recession fears and drag cyclicals lower. A surprisingly hawkish central bank remark can hit indices, sectors, and crowded trades at the same time. Overnight exposure means the trader is carrying not only stock specific risk, but also event risk from the macro calendar. This matters even more for traders who concentrate in a narrow group of names. A portfolio full of technology stocks may look diversified by ticker count, but it is still heavily exposed to one macro factor if rates move sharply. Overnight volatility often reveals these hidden correlations in a rude way.

The weekend effect

A Tuesday night position carries risk. A weekend position carries more. There are no regular trading sessions between Friday’s close and Monday’s open, but the world still goes on for 65+ hours, and macro news will appear. Political developments, military events, policy statements, commodity shocks, and company headlines can all pile up while most traders are inactive.

Compared to a single night, the weekend is a longer window for uncertainty to compound without the stabilizing function of regular market hours. A stock held over one night faces one night of event risk. A stock held from Friday to Monday faces 65+ hours where global markets, news desks, and social media can reshape sentiment.

That does not mean it is wrong to keep positions over the weekend. The point is that the distribution of outcomes becomes wider and this needs to be taken into account when you risk manage. The odds of a routine open may still be high, but the tail risk is worse. Traders who are comfortable holding medium sized positions from one day to the next are often far less comfortable holding the same size through a weekend once they have lived through a few ugly Monday gaps.

Global contagion and cross market spillover

US based traders sometimes behave as if action starts at 9:30 a.m. ET and markets sleep until then. This is a dangerous idea, because markets in other parts of the world are open, the global forex market is active, bond yields adjust, and commodity prices react to headlines in real time. By the time a US stock trader checks pre-market quotes for NYSE, a large part of the global risk transfer may already be done.

This matters because markets are linked more tightly during stress. A sharp drop in Japanese equities, a credit scare in the European Union, or a disorderly move in oil can spread through futures and ETFs long before the cash open in New York. A trader may hold a perfectly ordinary US position with no obvious overseas exposure, yet still wake up to lower prices because global funds are cutting risk broadly.

Contagion does not need to be dramatic to matter. Even a moderate overnight selloff in foreign equities can shift tone, pressure index futures, and weaken demand for risk assets at the US open. In calmer markets this may create only a small headwind. In nervous markets it can turn into a gap that invalidates the previous day’s chart structure before the first bell is heard.

Margin Calls and Forced Liquidation

Leveraged positions can turn overnight volatility from unpleasant into dangerous. A margined account allows larger positions, but that extra exposure cuts both ways. If a stock gaps lower overnight, account equity can fall below maintenance requirements before the trader has a chance to act. At that point, the broker may issue a margin call or liquidate positions to bring the account back into compliance. This is one of the less glamorous traps in swing trading because it has little to do with chart skill. The position may have been entered cleanly and managed according to plan. None of that matters if the account is overextended relative to gap risk. The broker’s priority is not preserving the trader’s thesis. It is controlling the broker’s own exposure.

Forced liquidation is especially painful because it tends to happen at bad prices and under stress. The trader loses not only money, but also control of execution. In practical terms, margin compresses room for error precisely when overnight markets are least forgiving. Many traders find out they were too leveraged only after the broker has already made that decision for them.

Examples of Risk Mitigation Strategies for Swing Traders

Conservative position sizing

The simplest defense against overnight risk is smaller size. That sounds obvious, which is probably why many traders ignore it. Yet position sizing does more to keep traders alive than almost any clever entry technique. A gap hurts less when the position is modest. It hurts a lot more when the account is leaning on a single name or a small cluster of correlated trades.

Smaller sizing does not eliminate gap risk, but it changes the consequences. A ten percent overnight move against a small position is frustrating. The same move against an oversized position can knock a trader off plan for weeks, either financially or mentally. Survival matters because swing trading is a repeated game. The trader who absorbs bad gaps and keeps operating has an edge over the trader who swings for the fences and gets carted off by one ugly open.

Refusing uncompensated risk

Many professional traders reduce or close positions before scheduled earnings. The logic is not that earnings cannot produce gains. They can, and sometimes dramatic ones. The logic is that the event changes the nature of the trade. Before the report, the trader may have a technical thesis. Into the report, the trader owns an event lottery ticket with uncertain odds and large possible price jumps.

Flattening a position 24 hours before earnings is a way of refusing uncompensated risk. There is no prize for being brave in front of a binary event. The market offers plenty of opportunities after the report, once the new information is public and price has settled enough to analyse again. Missing one gap up is usually cheaper than repeatedly absorbing gap downs across a year of trading.

The same principle applies more broadly to other scheduled landmines. If a stock faces a major regulatory decision, investor day, merger ruling, or major macro release that clearly affects the trade, standing aside is often the higher quality decision. Traders do not need to participate in every uncertain event just because it is on the calendar.

Diversification that actually diversifies

Diversification helps only when positions do not all fail together. Holding stocks in seven companies instead of one is not protection if all seven stock prices are driven by the same factor. A basket of semiconductors may look broad by ticker count and still behave like one trade during an overnight macro shock.

Real diversification spreads exposure across sectors, styles, geography, event calendars, and more. Reduce the risk of one gap down infecting the full book. This is less exciting than concentrated conviction, but it is often what keeps a swing trader in the game long-term. Overnight risk cannot be predicted reliably. It can only be spread, reduced, and hedged. A portfolio built with that in mind is less likely to be derailed by one earnings miss, one inflation print, or one overseas shock.

The practical question is simple. If the worst overnight headline in one area hits, how much of the account is affected at once? If the answer is “most of it,” the portfolio is not diversified in any meaningful sense.

Hedging with options

Options can convert unknown overnight risk into defined risk. A protective put gives the holder the right to sell at a strike price, which can place a floor under the loss on a long stock position. A collar combines a put with a covered call, reducing hedge cost in exchange for limiting upside. These structures are not free, and they are sometimes quite expensive, especially when implied volatility is elevated. But they provide something a stop-loss order cannot always provide overnight, which is contractual downside protection.

That makes options useful around known event risk. A trader who insists on holding through earnings, for example, may decide that paying for a put is the cost of staying in the trade. The hedge will reduce profit if the stock rallies, but it can stop a catastrophic gap from becoming an account level problem. The math may not always be attractive, but the risk profile is clearer. Of course, options introduce their own complications, including time decay, volatility pricing, and strike selection. So they are not a cure all. But at a basic level, they solve one important problem. They replace wishful thinking about stop execution with a predefined legal claim on downside protection.

How does a collar work?

A collar combines a put option and a call option:

- Protective put → sets a minimum exit price (downside protection)

- Covered call → generates income but caps upside

This way, you define a worst-case loss and a maximum profit for your long position. You also reduce (or sometimes eliminate) the cost of the hedge.

Example

- Let´s say you own 100 shares of XYZ stock. The current share price is $100, so the total position is $10,000.

- You buy a put option, with the strike price $95. The cost is $3 per share, for a total cost of $300 in total for your 100 shares. The put option gives you the right to sell the shares at $95, so you have capped the loss (downside protection).

- You also sell a covered call, i.e. a call option. The strike price is $110. The premium received is $2 per share, which is a total of $200 for 100 shares. This means that if the share price goes above $110 you must sell your shares at $110.

The put cost is $300 and the call income is $200. The net cost for this protection is thus $100.

Let´s now assume there is a big gap down, with the share price crashing to $70 over the weekend. Your put option lets you sell at $95, which means you lost $5 per share, which is $500 in total. $500 loss + the $100 net cost is a $600 loss. Despite the sharp decline in share price, you only took a $600 hit. If you had sold the shares at $70 instead, you would have lost $30 per share, for a total loss of $3,000.

Let´s look at a neutral scenario instead. The stock price is $100 at Friday close and $100 at Monday opening. Both your options expire out of the money. Your loss is the $100 net cost for the options.

Now, it is time to look at the best-case scenario. The stock jumps from $100 to $120 over the weekend. This means you call option gets exercised, and you must sell you shares at $110. Your profit on that sale is $10 per share, for a total of $1,000. The hedge cost was still $100 net cost. $1,000 profit minus $100 hedge cost is $900. Without the call option, you could have sold at $120 instead of $110, and this might feel annoying, but you still made a profit by selling at $110.

As you can see, a collar can help a swing trader manage overnight gaps in a way that stop-loss orders can not. A collar will cap your maximum profit, but it will also cap your downside, and can be worth it when news are on the horizon. Protective put options can be expensive, but the call option offsets that cost and makes the hedge more affordable.

Swing traders often use collars before earnings announcements, for weekends with macro uncertainty, and when sitting on unrealized gains they want to protect without closing the position right now. A collar turns an uncertain overnight position into a defined-risk trade within a span, since both the downside and the upside is capped. The reason why you agree to cap your upside is because it helps reduce the net cost of the hedge.